Strada Announces Partnership with NiCE CXone Read our blogpost →

Strada Announces Partnership with NiCE CXone

Read our blogpost →

Strada Announces Partnership with NiCE CXone Read our blogpost →

What Is Digitization in Insurance? A Simple Guide for 2026

Amir Prodensky

CEO

14 min read

A straightforward breakdown of digital tools reshaping insurance today.

I still remember when managing insurance policies meant endless paperwork, phone calls, and filing cabinets.

Today, things look completely different.

Digitization has turned all that chaos into clarity. It’s not just about going paperless. It’s about working smarter, faster, and more connected than ever.

Digitization in insurance means using digital tools to improve how insurers operate and serve customers. From AI to automation and data analytics, these technologies help teams make quicker decisions, personalize offers, and deliver better service around the clock.

Why does this matter so much now? Because customer expectations have changed. People want instant answers, simple claims, and personalized experiences, and insurtech startups are raising the bar.

Traditional insurers can’t afford to lag behind.

Digitization helps bridge that gap. It speeds up claims and underwriting, personalizes products, and enables 24/7 support that customers love.

Now that you know what digitization means, let’s look at how it’s changing the insurance world in real time.

How is digitization shaping the insurance industry today?

You’ll be surprised by how much digitization in the insurance sector is transforming everything right now. Across life, health, and cyber insurance, companies are speeding up their digital game.

In fact, 63% of insurers plan to be fully digitized by 2026. The insurtech market is booming, growing rapidly as new technologies reshape how insurers work and serve customers.

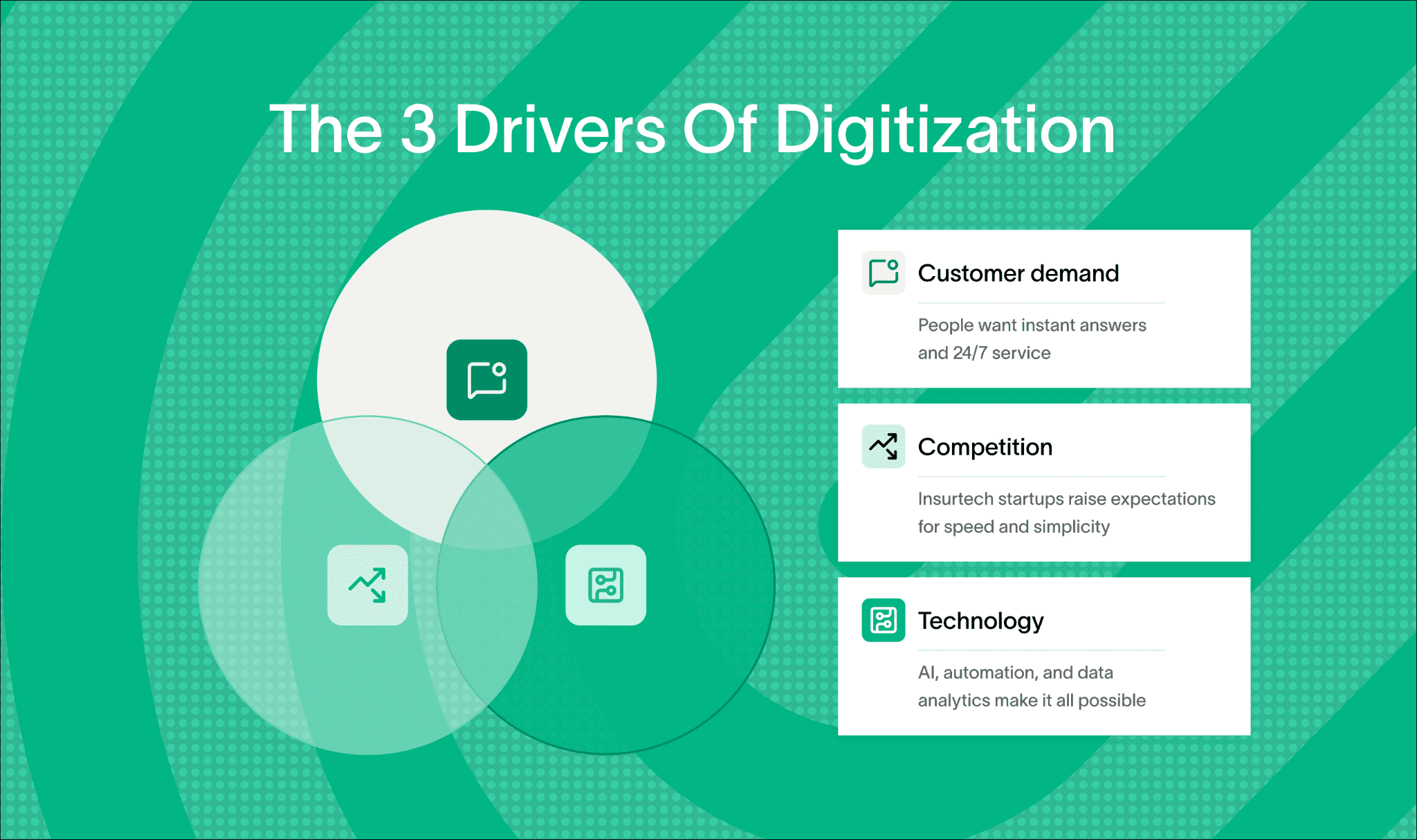

What’s driving this shift? It boils down to three key things: customer demand, tougher competition, and new technology.

Customers want faster, simpler service on their phones. Insurers face pressure to keep up with nimble startups and tech-savvy rivals.

Meanwhile, technologies like AI, blockchain, and IoT devices keep opening fresh ways to improve operations. Here are some practical examples of digital tools making a difference today:

Mobile apps that let you manage policies or file claims anytime, anywhere

Chatbots providing quick answers without waiting on hold

Automated underwriting to speed up approvals and reduce errors

Telematics for real-time risk assessment in auto insurance

Blockchain ensuring transparency and security in transactions

These tools boost speed, cut costs, and improve how risks get assessed. They’re also great for spotting fraud faster and keeping customers engaged with personalized experiences.

One standout example is Strada’s AI phone agents. They handle calls 24/7 for things like renewals, first notice of loss (claims intake), policy updates, and customer follow-ups. This not only ramps up efficiency but also helps keep customers happy and loyal.

Simply put, digitization in insurance is making the industry faster, smarter, and more customer-friendly. And if you’re wondering what’s next, expect even smoother, more connected experiences very soon.

So, what’s driving all this change? It starts with the tools behind the transformation. Let’s break down the key technologies that power modern insurance, from AI to automation and everything in between.

What digital technologies are insurers using?

When it comes to digitization in insurance, technology is the engine that drives efficiency, customer experience, and innovation. You’ll find that insurers today rely on a range of digital tools and platforms designed to simplify operations and deliver personalized service faster.

Here’s a straightforward breakdown of the core tech powering this transformation.

1. Artificial intelligence

First up, AI plays a huge role.

It enables predictive analytics that help insurers assess risks more accurately. AI automates underwriting, so policies get approved quicker without compromising quality. It’s also essential for fraud detection, flagging suspicious claims before they cause big losses.

On top of that, AI streamlines claims processing by analyzing documents and data faster than humans can.

2. Robotic process automation (RPA) and intelligent automation

Next, RPA and intelligent automation shave hours off repetitive tasks. These tools handle workflows like:

Data entry → bots pull and update client information instantly. No more manual typing.

Policy renewals → automated reminders and renewals keep customers engaged without staff chasing dates.

Billing and payments → systems generate invoices, send payment links, and confirm transactions automatically.

Document processing → AI scans forms, extracts key details, and files them where they belong.

Customer updates → automated workflows send status emails or texts right after each step.

The result? Happier teams and quicker turnaround times.

3. Chatbots and conversational AI

Customer service has gone digital too.

Chatbots and conversational AI provide 24/7 support for policy questions, claims updates, and onboarding. For example, tools like Artificial Solutions and Lemonade’s AI chatbot engage customers instantly, answering common queries and guiding them through process steps without waiting on hold.

One impressive example in conversational AI is Strada’s platform, which uses insurance-specific AI models trained on industry terminology. It handles calls covering quote intake, lead qualification, renewals, claims, and policy servicing with ease.

Best of all, it integrates smoothly with CRM and AMS systems, creating a seamless experience for both agents and customers.

4. Telematics and IoT devices

If you want real personalization, look no further than telematics and IoT devices. By tracking driving behavior or home conditions, insurers offer usage-based policies that reward safe habits with lower premiums.

Companies like Octo Telematics and T-Sense lead the way here, giving both insurers and policyholders real-time insights.

5. Blockchain and smart contracts

Security and transparency also get a boost from blockchain and smart contracts. These technologies make policy and claim management more secure and transparent by recording transactions on distributed ledgers.

Platforms such as Ethereum-based solutions and IBM Blockchain reduce paperwork and minimize disputes.

6. Digital Adoption Platforms (DAPs)

To help agents get the most from these digital upgrades, many insurers turn to Digital Adoption Platforms like Whatfix. These platforms train employees on new software quickly, improving productivity and encouraging tech use across the board.

7. Cloud, APIs, and modern architecture

Digitization isn’t just about isolated tools. It’s also about how companies plan and deploy them. Many insurers use an AI roadmap approach: identifying use cases, running pilot projects, then scaling successful solutions.

Meanwhile, modernizing legacy systems often relies on API-first architecture, microservices, and cloud-native transformation to increase flexibility. Leading cloud platforms like AWS, Microsoft Azure, and Google Cloud provide the scalability and security insurance companies need.

Of course, technology alone doesn’t make the magic happen.

It’s what you do with it.

Next, we’ll explore how these digital tools are completely reinventing the customer experience, making it faster, smoother, and more personal than ever.

How is customer experience transforming with digitization?

Today, it’s all about a digital-first, omnichannel journey. Instead of sticking to phone calls or in-person visits, you can now manage your policies through mobile apps, online portals, and self-service tools anytime, anywhere.

For example, platforms like Policybazaar and Insurify make comparing policies and buying insurance simple and quick without the usual hassle.

And this shift goes beyond convenience. AI is stepping in to make things smarter and more personalized. Here’s how it’s changing the game:

Predictive insights → AI anticipates customer needs, like when they’re likely to renew or file a claim.

Smarter pricing → machine learning adjusts premiums based on real behavior and risk data.

Instant service → chatbots and AI assistants provide quick, accurate responses 24/7.

Tailored offers → algorithms match customers with the right products in seconds.

Faster decisions → AI analyzes documents and verifies information automatically, cutting delays.

With AI working behind the scenes, every interaction becomes faster, more accurate, and far more relevant to each customer. Plus, AI-powered recommendation engines suggest the best policies suited to your needs.

Dynamic pricing adjusts costs based on real-time data, making sure you get competitive deals. Natural language processing (NLP) and sentiment analysis help understand your questions and feedback more accurately, offering faster, tailored responses that keep you engaged.

Now, here’s where it gets really useful: digitization speeds up service. You can submit claims in real-time just by uploading images or videos from your smartphone. No more waiting in lines or mailing documents.

Digital signatures mean you can sign contracts instantly, without printing a single page. To make digital signatures part of your everyday workflow, here’s a quick step-by-step guide:

Step | What to do | Why it matters |

1. Choose a platform | Pick a trusted tool like DocuSign, Adobe Sign, or HelloSign. | Ensures legal compliance and security. |

2. Upload your document | Add contracts, policies, or claim forms directly from your computer or cloud storage. | Saves time and centralizes files. |

3. Add signature fields | Drag and drop where signatures, initials, or dates should appear. | Makes signing clear and easy for clients. |

4. Send for signature | Email the document securely to your client or team member. | Cuts delays from printing, scanning, or mailing. |

5. Track progress | Get instant notifications when someone signs or opens your document. | Keeps you informed and speeds up approvals. |

6. Store and sync | Save completed documents automatically in your CRM or AMS. | Keeps records organized and easy to retrieve. |

Need advice? Many insurers offer virtual consultations via video directly integrated into their portals – helpful and hassle-free.

Another game-changer is chatbots and conversational AI. These tools provide 24/7 support, answering common questions anytime, helping you avoid hold times or searching through FAQs.

Strada is a great example of this transformation in action. They offer zero-hold-time phone service and smart call scheduling with intelligent retries, which means you get connected faster and more often. Their personalized, trusted interactions boost customer loyalty and keep you coming back.

Here’s what makes Strada stand out in everyday use:

Faster connections → calls route instantly to the right agent or AI assistant; no waiting.

Smarter follow-ups → missed calls trigger automatic retries and reminders, so no lead slips away.

Personal touch → AI tailors conversations based on customer history and preferences.

Consistent support → works 24/7 across phone and SMS, so customers always get help when they need it.

Happier teams → agents handle fewer repetitive calls and focus on high-value interactions.

Together, these features turn every call into a smooth, personalized experience, boosting satisfaction, efficiency, and long-term loyalty.

Which brings us to design. Insurers are making their apps and websites easier to use. They follow proven UX/UI frameworks like Material Design or Human Interface Guidelines, so everything feels intuitive and smooth.

Plus, they continuously improve features using agile methods and DevOps to keep you satisfied and reduce the chances you’ll switch providers.

With these changes, insurance digitization is not just about technology. It’s about making your experience easier, faster, and more personal every step of the way.

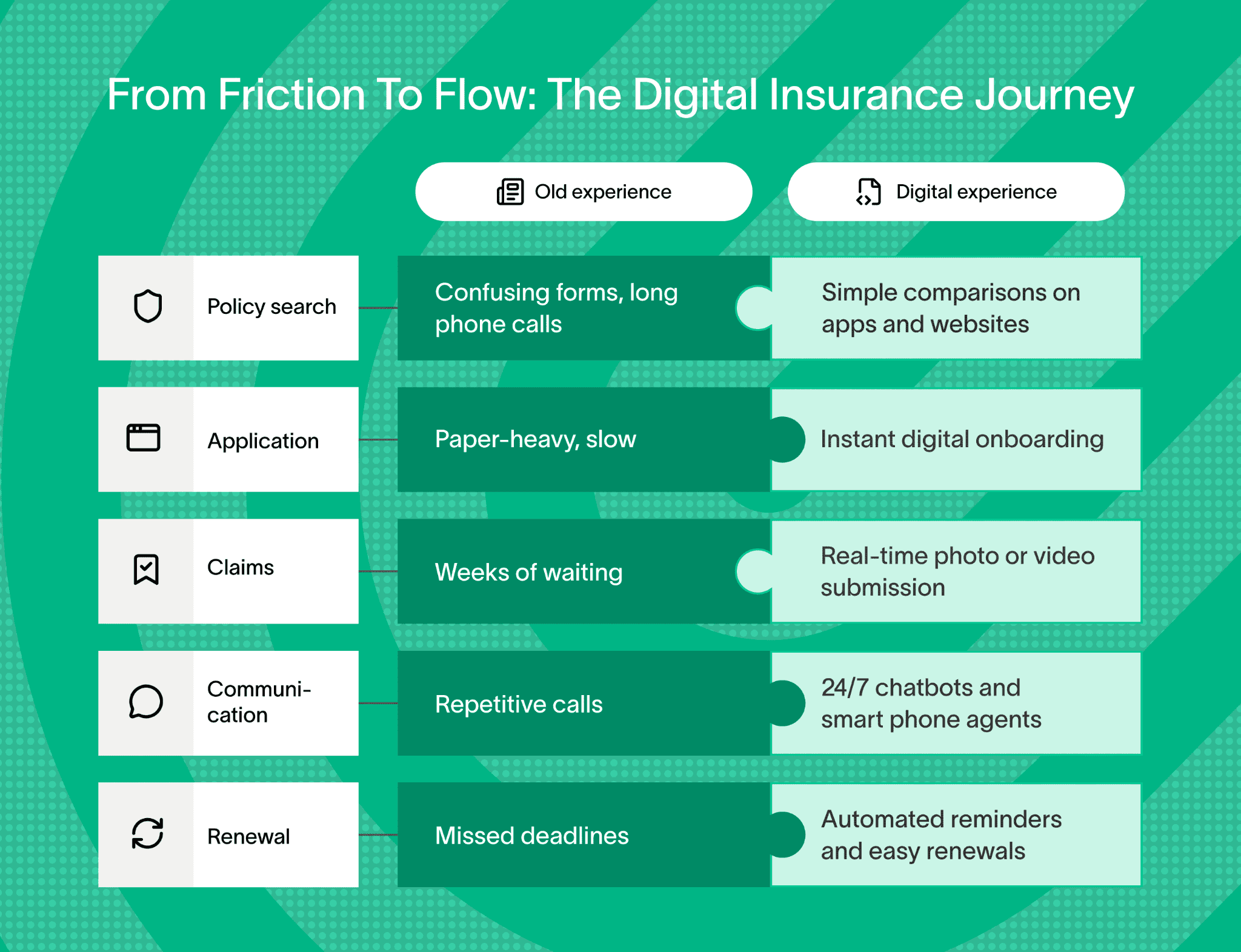

You can really see the difference when you look at the customer journey itself. Here’s what that evolution looks like in action.

But it’s not just customers who benefit. Digitization also transforms day-to-day operations, cutting manual work and boosting efficiency.

Let’s see how insurers are using digital tools to streamline claims, underwriting, and servicing.

How does digitization improve insurance operations?

You’ll be amazed at how digitization turbocharges insurance operations.

First, by automating manual tasks, insurers cut claims processing times drastically, from around 30 days to less than 15. This speed-up doesn’t just make customers happier; it also lowers human errors and helps spot fraud faster.

For example, AI-powered tools like Shift Technology and FRISS analyze patterns to catch suspicious claims early, protecting your bottom line. Next up, AI improves underwriting and risk assessment by digging into mountains of historical data.

No matter if it’s predicting the impact of natural disasters or profiling health risks, AI algorithms provide sharper, data-backed insights.

This means better pricing accuracy and smarter decisions in less time.

Digitization also brings RPA into play through platforms like UiPath and Automation Anywhere. These bots handle repetitive tasks such as document sorting, claim form parsing, and workflow approvals.

One standout tool is Strada Workflows – an AI platform that instantly turns call outcomes into automated actions across CRM, AMS, and policy systems. It streamlines tasks like renewals follow-up, claim file creation, payment recovery, and certificate issuance to reduce busywork and boost your team’s productivity.

Plus, NLP helps machines understand insurance documents and customer communications, speeding everything up through insurance document digitization without sacrificing accuracy.

Here’s a simple list of key automation benefits you’ll see:

Faster claims and policy workflows (with insurance policy digitization)

Reduced manual errors and fraud detection

Smarter risk assessment and underwriting

Lower operational costs from less manual labor and cloud infrastructure savings

Plus, switching to cloud systems slashes expenses tied to on-premise hardware. It also boosts how flexibly insurers can scale technology to meet demand. But there’s a catch: integrating new digital tools with old legacy systems is tricky.

Here’s how you can make integration smoother:

Start small → pick one process or module to modernize first instead of overhauling everything.

Use the strangler pattern → gradually replace legacy components with modern ones while keeping systems running.

Refactor step by step → clean up old code in small chunks to reduce risks and improve performance.

Containerize apps → tools like Docker and Kubernetes isolate workloads, making deployment and scaling easier.

Connect via APIs → use API gateways to let new and old systems talk without deep rewrites.

Test continuously → run automated tests to catch issues early and avoid downtime.

With these steps, you modernize confidently, keeping your operations stable while upgrading to smarter, faster tools.

Alongside tech upgrades, strong data governance frameworks like DAMA-DMBOK ensure your data stays accurate and compliant, which is crucial when dealing with sensitive insurance info. This keeps your operations smooth and trustworthy.

Still, going digital isn’t always smooth sailing. Many insurers run into hurdles like legacy systems or slow adoption. Here’s what’s holding companies back and how to overcome those challenges.

What challenges do insurers face in digitization?

Digitizing insurance processes comes with real challenges, but understanding them will help you tackle them head-on.

You’ll find that cybersecurity tops the list.

Insurers handle sensitive data, so strong security is a must. This means using encryption like AES-256, multi-factor authentication (MFA), role-based access controls, and intrusion detection systems (IDS/IPS). Zero-trust architectures also keep threats at bay by assuming no user or device is automatically trusted.

Next, there’s the complexity of regulatory compliance. You need to navigate laws like GDPR and CCPA, plus insurance-specific rules such as eIDAS and Solvency II. These regulations keep evolving, so staying updated and flexible is key.

Trying to bring new digital tools into old legacy systems can feel like fitting a square peg in a round hole. To smooth this, many insurers use:

Tool type | What it does | Best for | Example platforms |

API gateway | Acts as a single entry point for different systems to communicate securely. | Connecting cloud apps, CRMs, and external services easily. | Kong, Apigee, AWS API Gateway |

Middleware | Sits between systems to translate and route data automatically. | Integrating legacy databases with new digital tools. | MuleSoft, Zapier, Workato |

Enterprise Service Bus (ESB) | Connects multiple enterprise systems with centralized message handling. | Large-scale operations needing high reliability and complex workflows. | IBM Integration Bus, Dell Boomi, WSO2 |

These tools help modernize systems in phases, making the transition manageable. Hybrid cloud adoption also offers a flexible way to scale up digital capabilities without a full overhaul.

Culture-wise, shifting to a digital mindset matters. It’s about agility and teamwork. Frameworks can guide this change. Here are a few that can help shape your digital culture:

SAFe (Scaled Agile Framework) → great for aligning teams, improving collaboration, and managing complex digital programs.

ADKAR Model → focuses on individual change (Awareness, Desire, Knowledge, Ability, and Reinforcement) to help teams adapt smoothly.

Lean Change Management → encourages quick feedback loops and experimentation when rolling out new digital initiatives.

Scrum → ideal for smaller teams running iterative projects with frequent progress reviews.

Design Thinking → keeps your digital transformation customer-focused through empathy, prototyping, and testing.

And, you’ll want to foster data literacy so everyone understands the value of data.

Plus, encouraging continuous innovation through hackathons or innovation labs keeps ideas flowing and teams engaged.

Your workforce will need new skills, too. Think data science, AI oversight, and digital engagement roles. Change management comes into play here, supported by ongoing learning platforms like Coursera and Udemy for Business. These help keep skills fresh and relevant.

Also, solutions like Strada offer enterprise-grade security with SOC 2 Type 2 certifications, customer data isolation, regular penetration tests, and a privacy-first approach in their training data and large language models. These features meet the strict security and compliance standards insurers need.

By tackling these challenges with the right tools and mindset, you’ll navigate digitization in the insurance industry smoothly and successfully.

Once you know the roadblocks (and the way of overcoming challenges in insurance digitization), it’s time to plan your route forward. You’ll learn how to create a clear digital strategy that fits your business goals and helps your teams adapt with confidence.

How can insurers craft a strategic approach to digital transformation?

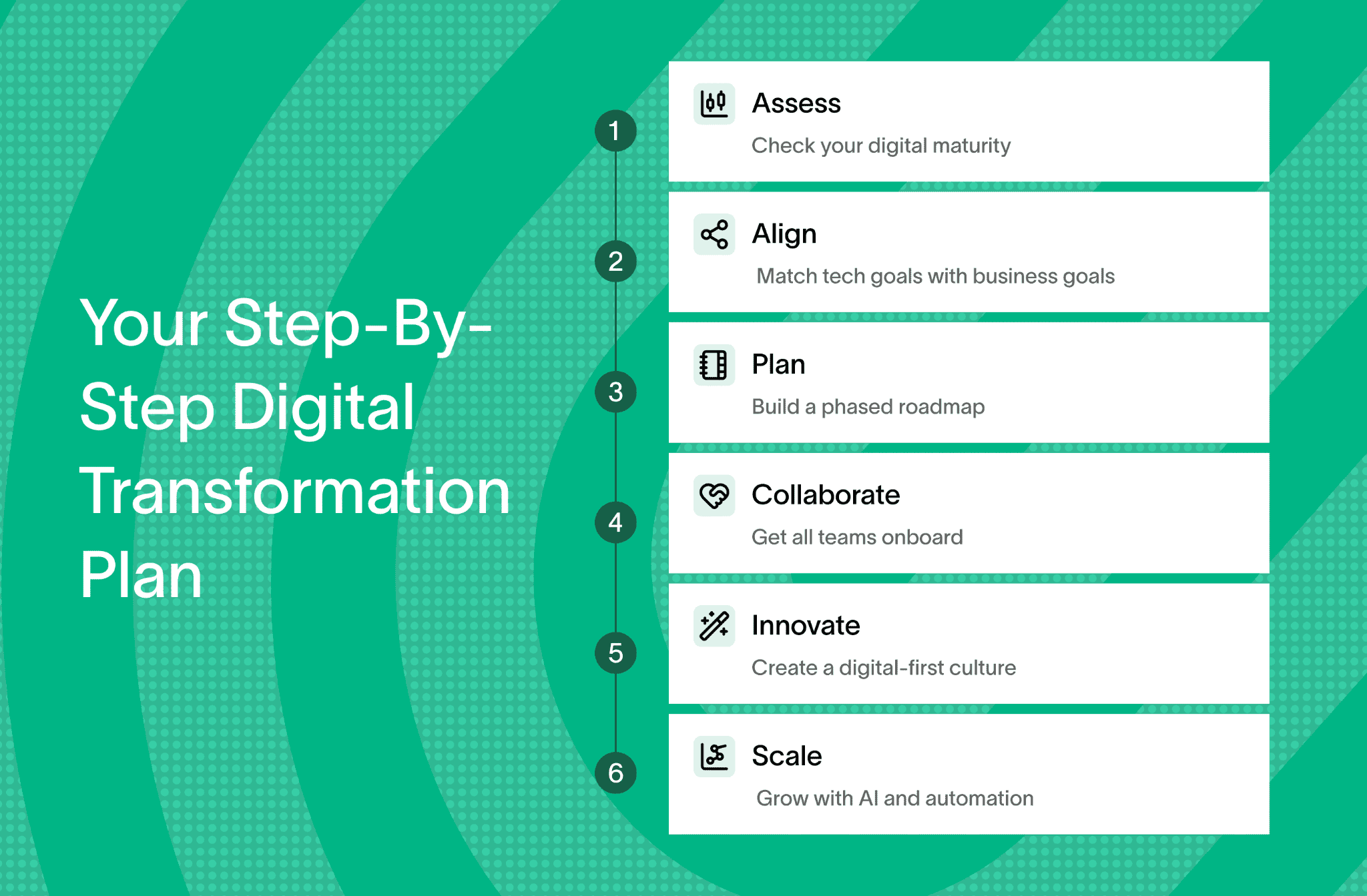

If you’re ready to “embrace” digitization in the insurance industry, taking a thoughtful, step-by-step approach is key. It’s all about reshaping how your entire organization works to meet future challenges and customer expectations.

Here’s a simple visual to keep your digital journey on track.

And here’s how to build a strong strategy that aligns with your goals and drives measurable results.

Step 1: Assess your digital maturity

Start by understanding where your company stands today.

Use frameworks like the Deloitte Digital Maturity Model to evaluate your current capabilities across technology, processes, and culture.

Here’s how to put it into action:

Assess your baseline. Review where you stand in key areas like strategy, technology, operations, and customer engagement.

Identify gaps. Pinpoint where your digital capabilities fall short, such as outdated tools, slow processes, or low data use.

Prioritize improvements. Focus first on areas that will deliver the biggest business impact, like automation or data analytics.

Set measurable goals. Define clear KPIs, e.g., faster claim turnaround or higher customer satisfaction.

Reassess regularly. Repeat the evaluation every 6–12 months to track progress and adjust your strategy as technology evolves.

This assessment highlights your strengths and gaps, giving you a clear baseline for planning. Think of it as a health check for your digital readiness.

Without this, you risk jumping into solutions that don’t fit or missing critical areas that need improvement.

Step 2: Align strategy with business goals

Next up, sync your digital ambitions with your core business objectives:

Are you focused on improving customer experience?

Reducing claims processing time?

Expanding into new markets?

Make sure your digital strategy supports these goals directly. This alignment ensures every digital initiative adds clear value, avoiding wasted resources on projects that don’t advance your business.

Step 3: Develop a phased implementation roadmap

Trying to do everything at once is a recipe for overwhelm. Instead, outline a phased rollout:

Pilot programs → test solutions on a small scale to learn quickly and adjust.

Scaling → expand successful pilots across departments or processes.

Continuous feedback → keep iterating based on user input and performance data.

This staged approach keeps risk low and momentum high as you grow your digital capabilities.

Step 4: Foster cross-functional collaboration

Digital transformation succeeds when teams work together seamlessly. Encourage collaboration between IT, business units, compliance, and customer service teams.

Using Agile frameworks like Scrum or Kanban can help you stay flexible and responsive. These methodologies promote regular check-ins, rapid problem-solving, and transparency.

Collaborative platforms such as Jira, Confluence, or Microsoft Teams are invaluable here. They keep everyone on the same page, organizing tasks, documentation, and communications in one place.

Step 5: Build a digital culture focused on innovation

Technology alone won’t transform your business. You need a culture that embraces innovation and experimentation. Set up innovation labs or sandbox environments where employees can test new ideas without fear of failure.

Encourage ongoing learning with resources like LinkedIn Learning or Lynda. Upskilling your team continuously equips them to handle new tools and changing workflows confidently.

Step 6: Invest in scalable AI solutions

Start by exploring scalable AI services, such as generative AI from OpenAI GPT models or Google Vertex AI, which can be accessed as a service without heavy upfront development.

For tailored solutions, consider platforms like Microsoft Azure AI or AWS SageMaker to build custom AI models suited to your unique insurance needs. These tools can automate underwriting, claims processing, risk assessment, and more.

For example, if you're looking into practical ways to transform operations with AI, solutions like Strada show how combining AI with workflow automation can boost efficiency and accuracy. If you’re ready to bring AI to life in your insurance operations, here’s a simple step-by-step way to get started with Strada:

Step 6.1: Identify your use cases.

Start small by choosing one or two high-impact areas. Here are a few great use cases to begin with:

Quote intake → capture customer details, qualify leads, and submit data directly into your CRM or AMS.

Renewal reminders → automatically reach out to policyholders before expiration and schedule follow-up calls for your agents.

Claims intake (FNOL) → collect first notice of loss details 24/7, assign adjusters, and trigger next steps instantly.

Payment recovery → follow up with customers who’ve promised payments and send automated reminders if needed.Certificate issuance → process certificate requests automatically and sync updates across your CRM and policy systems.

Lead routing → assign incoming leads based on region, product type, or agent expertise without manual work.

These processes often involve repetitive calls that Strada’s AI agents can easily automate.

Step 6.2: Connect your systems.

Strada integrates seamlessly with your CRM, AMS, and policy systems, so your data flows automatically. Work with your IT or operations team to connect Strada to tools like HubSpot, Salesforce, or Applied Epic using its built-in APIs.

Step 6.3: Configure workflows.

Next, set up your first automation workflows.

Strada Workflows can trigger actions like scheduling follow-ups, sending renewal reminders, or updating CRM records instantly after a call ends.

Step 6.4: Train and test your AI agents.

Use Strada’s onboarding support to train the AI on your product types, call scripts, and business rules. Then, run pilot calls to make sure the responses sound natural and accurate.

Step 6.5: Monitor and scale.

Once live, use Strada’s analytics dashboard to track performance – monitor metrics like call resolution rate, average handling time, and follow-up success.

When you’re confident, expand AI coverage to more lines of business.

In just a few weeks, you’ll see how Strada reduces manual tasks, improves response times, and keeps your agents focused on closing deals instead of chasing paperwork.

Step 7: Prioritize workforce training and performance monitoring

Your investment in technology won't pay off without an informed, engaged workforce. Use digital adoption platforms (such as Whatfix or WalkMe) to provide easy, on-the-job training that helps employees navigate new tools smoothly.

Track progress using analytics platforms like Tableau or Power BI. AI performance dashboards can give you real-time insights into how your AI systems perform, letting you spot issues or opportunities quickly.

Building a digital strategy doesn’t stop at your own systems. The smartest insurers are now connecting with partners (brokers, reinsurers, and tech providers) to share data and innovate together.

Let’s see how these ecosystems work in practice.

How can insurers use advanced data ecosystems and partnerships?

First up, building secure data lakes and warehouses is key.

Platforms like Snowflake and Databricks help insurers gather all types of data – from structured databases to unstructured files like emails or IoT sensor data – into one place. This consolidation makes it easier to analyze and find insights quickly.

Next, collaboration matters. Here’s how to make that collaboration work smoothly:

Use open APIs → allow systems from different partners to communicate securely and in real time.

Adopt standardized data formats → rely on formats like JSON or XML to keep information consistent and readable across platforms.

Implement secure authentication → use OAuth 2.0 or token-based access to protect shared data.

Leverage data exchange hubs → platforms like ACORD or industry-specific data exchanges simplify collaboration between carriers and brokers.

Track data flows → set up dashboards to monitor which partners access what data – keeping everything transparent and compliant.

This openness speeds up insurance customer onboarding digitization and creates a fuller picture of risk. Plus, data marketplaces and open data initiatives expand data sources even more. They bring in fresh, external info that sharpens risk models, making them more accurate.

Some great examples come from partnerships with tech giants. Take AWS Data Exchange and Google Cloud’s insurance programs. They provide curated, high-quality datasets and tools to help insurers innovate faster and smarter. These collaborations act as a bridge to a broader ecosystem where data flows securely and efficiently.

Of course, all this data sharing needs strong frameworks to keep info safe and respecting privacy. Techniques like differential privacy and federated learning let insurers analyze data without exposing personal details. Consent management frameworks ensure customers stay in control of their data.

Finally, platforms like Strada seamlessly fit into this ecosystem. Thanks to open APIs, Strada’s conversational AI insights feed directly into enterprise analytics, CRM systems, or customer data hubs.

This integration helps insurers make smarter, data-driven decisions at every step.

We’ve covered a lot, from new technologies to smarter partnerships. Now, let’s bring it all together and see what the future of digitization means for your insurance business.

How will digitization shape your next move?

Digitization in insurance isn’t just about adopting new tech. It’s about transforming how you work and connect with customers. In 2026 and beyond, the winners will be the insurers who act fast, stay flexible, and put customer experience first.

Here’s how to make it happen:

Start small, scale smart. Pick one process (like claims, renewals, or quote intake) and digitize it first.

Use AI and automation where it matters most. Free your team from repetitive work so they can focus on clients.

Break down data silos. Connect systems through APIs to keep information flowing across departments and partners.

Keep your people on board. Train teams early, communicate clearly, and celebrate small wins.

Measure and adapt. Track KPIs, review progress, and adjust quickly to stay ahead.

Platforms like Strada make this transformation easier. Its AI-driven phone agents automate calls, follow-ups, and workflows, so your team spends more time closing deals and less time on busywork.

Ready to see how it works? Book a Strada demo and discover how automation can help your insurance business move faster, serve better, and grow smarter.

Frequently Asked Questions

What’s the quickest way for insurers to start digitizing without a huge budget?

Begin with small wins—automate one process like renewals or FNOL intake using low-code tools or AI phone agents. This gives fast ROI without major IT overhaul.

How long does a typical insurance digitization project take?

Framer is a design tool that allows you to design websites on a freeform canvas, and then publish them as websites with a single click.

What’s the biggest mistake insurers make when adopting new digital tools?

Framer is a design tool that allows you to design websites on a freeform canvas, and then publish them as websites with a single click.

What KPIs should insurers track to measure digitization success?

Framer is a design tool that allows you to design websites on a freeform canvas, and then publish them as websites with a single click.

How do insurers avoid overwhelming their staff with new technologies?

Framer is a design tool that allows you to design websites on a freeform canvas, and then publish them as websites with a single click.

Table of Contents

Carriers, MGAs, and brokers scale revenue-driving phone calls with Strada's conversational AI platform.

Start scaling with voice AI agents today

Join innovative carriers and MGAs transforming their calls with Strada.

What Is Digitization in Insurance? A Simple Guide for 2026

Amir Prodensky

CEO

14 min read

A straightforward breakdown of digital tools reshaping insurance today.

I still remember when managing insurance policies meant endless paperwork, phone calls, and filing cabinets.

Today, things look completely different.

Digitization has turned all that chaos into clarity. It’s not just about going paperless. It’s about working smarter, faster, and more connected than ever.

Digitization in insurance means using digital tools to improve how insurers operate and serve customers. From AI to automation and data analytics, these technologies help teams make quicker decisions, personalize offers, and deliver better service around the clock.

Why does this matter so much now? Because customer expectations have changed. People want instant answers, simple claims, and personalized experiences, and insurtech startups are raising the bar.

Traditional insurers can’t afford to lag behind.

Digitization helps bridge that gap. It speeds up claims and underwriting, personalizes products, and enables 24/7 support that customers love.

Now that you know what digitization means, let’s look at how it’s changing the insurance world in real time.

How is digitization shaping the insurance industry today?

You’ll be surprised by how much digitization in the insurance sector is transforming everything right now. Across life, health, and cyber insurance, companies are speeding up their digital game.

In fact, 63% of insurers plan to be fully digitized by 2026. The insurtech market is booming, growing rapidly as new technologies reshape how insurers work and serve customers.

What’s driving this shift? It boils down to three key things: customer demand, tougher competition, and new technology.

Customers want faster, simpler service on their phones. Insurers face pressure to keep up with nimble startups and tech-savvy rivals.

Meanwhile, technologies like AI, blockchain, and IoT devices keep opening fresh ways to improve operations. Here are some practical examples of digital tools making a difference today:

Mobile apps that let you manage policies or file claims anytime, anywhere

Chatbots providing quick answers without waiting on hold

Automated underwriting to speed up approvals and reduce errors

Telematics for real-time risk assessment in auto insurance

Blockchain ensuring transparency and security in transactions

These tools boost speed, cut costs, and improve how risks get assessed. They’re also great for spotting fraud faster and keeping customers engaged with personalized experiences.

One standout example is Strada’s AI phone agents. They handle calls 24/7 for things like renewals, first notice of loss (claims intake), policy updates, and customer follow-ups. This not only ramps up efficiency but also helps keep customers happy and loyal.

Simply put, digitization in insurance is making the industry faster, smarter, and more customer-friendly. And if you’re wondering what’s next, expect even smoother, more connected experiences very soon.

So, what’s driving all this change? It starts with the tools behind the transformation. Let’s break down the key technologies that power modern insurance, from AI to automation and everything in between.

What digital technologies are insurers using?

When it comes to digitization in insurance, technology is the engine that drives efficiency, customer experience, and innovation. You’ll find that insurers today rely on a range of digital tools and platforms designed to simplify operations and deliver personalized service faster.

Here’s a straightforward breakdown of the core tech powering this transformation.

1. Artificial intelligence

First up, AI plays a huge role.

It enables predictive analytics that help insurers assess risks more accurately. AI automates underwriting, so policies get approved quicker without compromising quality. It’s also essential for fraud detection, flagging suspicious claims before they cause big losses.

On top of that, AI streamlines claims processing by analyzing documents and data faster than humans can.

2. Robotic process automation (RPA) and intelligent automation

Next, RPA and intelligent automation shave hours off repetitive tasks. These tools handle workflows like:

Data entry → bots pull and update client information instantly. No more manual typing.

Policy renewals → automated reminders and renewals keep customers engaged without staff chasing dates.

Billing and payments → systems generate invoices, send payment links, and confirm transactions automatically.

Document processing → AI scans forms, extracts key details, and files them where they belong.

Customer updates → automated workflows send status emails or texts right after each step.

The result? Happier teams and quicker turnaround times.

3. Chatbots and conversational AI

Customer service has gone digital too.

Chatbots and conversational AI provide 24/7 support for policy questions, claims updates, and onboarding. For example, tools like Artificial Solutions and Lemonade’s AI chatbot engage customers instantly, answering common queries and guiding them through process steps without waiting on hold.

One impressive example in conversational AI is Strada’s platform, which uses insurance-specific AI models trained on industry terminology. It handles calls covering quote intake, lead qualification, renewals, claims, and policy servicing with ease.

Best of all, it integrates smoothly with CRM and AMS systems, creating a seamless experience for both agents and customers.

4. Telematics and IoT devices

If you want real personalization, look no further than telematics and IoT devices. By tracking driving behavior or home conditions, insurers offer usage-based policies that reward safe habits with lower premiums.

Companies like Octo Telematics and T-Sense lead the way here, giving both insurers and policyholders real-time insights.

5. Blockchain and smart contracts

Security and transparency also get a boost from blockchain and smart contracts. These technologies make policy and claim management more secure and transparent by recording transactions on distributed ledgers.

Platforms such as Ethereum-based solutions and IBM Blockchain reduce paperwork and minimize disputes.

6. Digital Adoption Platforms (DAPs)

To help agents get the most from these digital upgrades, many insurers turn to Digital Adoption Platforms like Whatfix. These platforms train employees on new software quickly, improving productivity and encouraging tech use across the board.

7. Cloud, APIs, and modern architecture

Digitization isn’t just about isolated tools. It’s also about how companies plan and deploy them. Many insurers use an AI roadmap approach: identifying use cases, running pilot projects, then scaling successful solutions.

Meanwhile, modernizing legacy systems often relies on API-first architecture, microservices, and cloud-native transformation to increase flexibility. Leading cloud platforms like AWS, Microsoft Azure, and Google Cloud provide the scalability and security insurance companies need.

Of course, technology alone doesn’t make the magic happen.

It’s what you do with it.

Next, we’ll explore how these digital tools are completely reinventing the customer experience, making it faster, smoother, and more personal than ever.

How is customer experience transforming with digitization?

Today, it’s all about a digital-first, omnichannel journey. Instead of sticking to phone calls or in-person visits, you can now manage your policies through mobile apps, online portals, and self-service tools anytime, anywhere.

For example, platforms like Policybazaar and Insurify make comparing policies and buying insurance simple and quick without the usual hassle.

And this shift goes beyond convenience. AI is stepping in to make things smarter and more personalized. Here’s how it’s changing the game:

Predictive insights → AI anticipates customer needs, like when they’re likely to renew or file a claim.

Smarter pricing → machine learning adjusts premiums based on real behavior and risk data.

Instant service → chatbots and AI assistants provide quick, accurate responses 24/7.

Tailored offers → algorithms match customers with the right products in seconds.

Faster decisions → AI analyzes documents and verifies information automatically, cutting delays.

With AI working behind the scenes, every interaction becomes faster, more accurate, and far more relevant to each customer. Plus, AI-powered recommendation engines suggest the best policies suited to your needs.

Dynamic pricing adjusts costs based on real-time data, making sure you get competitive deals. Natural language processing (NLP) and sentiment analysis help understand your questions and feedback more accurately, offering faster, tailored responses that keep you engaged.

Now, here’s where it gets really useful: digitization speeds up service. You can submit claims in real-time just by uploading images or videos from your smartphone. No more waiting in lines or mailing documents.

Digital signatures mean you can sign contracts instantly, without printing a single page. To make digital signatures part of your everyday workflow, here’s a quick step-by-step guide:

Step | What to do | Why it matters |

1. Choose a platform | Pick a trusted tool like DocuSign, Adobe Sign, or HelloSign. | Ensures legal compliance and security. |

2. Upload your document | Add contracts, policies, or claim forms directly from your computer or cloud storage. | Saves time and centralizes files. |

3. Add signature fields | Drag and drop where signatures, initials, or dates should appear. | Makes signing clear and easy for clients. |

4. Send for signature | Email the document securely to your client or team member. | Cuts delays from printing, scanning, or mailing. |

5. Track progress | Get instant notifications when someone signs or opens your document. | Keeps you informed and speeds up approvals. |

6. Store and sync | Save completed documents automatically in your CRM or AMS. | Keeps records organized and easy to retrieve. |

Need advice? Many insurers offer virtual consultations via video directly integrated into their portals – helpful and hassle-free.

Another game-changer is chatbots and conversational AI. These tools provide 24/7 support, answering common questions anytime, helping you avoid hold times or searching through FAQs.

Strada is a great example of this transformation in action. They offer zero-hold-time phone service and smart call scheduling with intelligent retries, which means you get connected faster and more often. Their personalized, trusted interactions boost customer loyalty and keep you coming back.

Here’s what makes Strada stand out in everyday use:

Faster connections → calls route instantly to the right agent or AI assistant; no waiting.

Smarter follow-ups → missed calls trigger automatic retries and reminders, so no lead slips away.

Personal touch → AI tailors conversations based on customer history and preferences.

Consistent support → works 24/7 across phone and SMS, so customers always get help when they need it.

Happier teams → agents handle fewer repetitive calls and focus on high-value interactions.

Together, these features turn every call into a smooth, personalized experience, boosting satisfaction, efficiency, and long-term loyalty.

Which brings us to design. Insurers are making their apps and websites easier to use. They follow proven UX/UI frameworks like Material Design or Human Interface Guidelines, so everything feels intuitive and smooth.

Plus, they continuously improve features using agile methods and DevOps to keep you satisfied and reduce the chances you’ll switch providers.

With these changes, insurance digitization is not just about technology. It’s about making your experience easier, faster, and more personal every step of the way.

You can really see the difference when you look at the customer journey itself. Here’s what that evolution looks like in action.

But it’s not just customers who benefit. Digitization also transforms day-to-day operations, cutting manual work and boosting efficiency.

Let’s see how insurers are using digital tools to streamline claims, underwriting, and servicing.

How does digitization improve insurance operations?

You’ll be amazed at how digitization turbocharges insurance operations.

First, by automating manual tasks, insurers cut claims processing times drastically, from around 30 days to less than 15. This speed-up doesn’t just make customers happier; it also lowers human errors and helps spot fraud faster.

For example, AI-powered tools like Shift Technology and FRISS analyze patterns to catch suspicious claims early, protecting your bottom line. Next up, AI improves underwriting and risk assessment by digging into mountains of historical data.

No matter if it’s predicting the impact of natural disasters or profiling health risks, AI algorithms provide sharper, data-backed insights.

This means better pricing accuracy and smarter decisions in less time.

Digitization also brings RPA into play through platforms like UiPath and Automation Anywhere. These bots handle repetitive tasks such as document sorting, claim form parsing, and workflow approvals.

One standout tool is Strada Workflows – an AI platform that instantly turns call outcomes into automated actions across CRM, AMS, and policy systems. It streamlines tasks like renewals follow-up, claim file creation, payment recovery, and certificate issuance to reduce busywork and boost your team’s productivity.

Plus, NLP helps machines understand insurance documents and customer communications, speeding everything up through insurance document digitization without sacrificing accuracy.

Here’s a simple list of key automation benefits you’ll see:

Faster claims and policy workflows (with insurance policy digitization)

Reduced manual errors and fraud detection

Smarter risk assessment and underwriting

Lower operational costs from less manual labor and cloud infrastructure savings

Plus, switching to cloud systems slashes expenses tied to on-premise hardware. It also boosts how flexibly insurers can scale technology to meet demand. But there’s a catch: integrating new digital tools with old legacy systems is tricky.

Here’s how you can make integration smoother:

Start small → pick one process or module to modernize first instead of overhauling everything.

Use the strangler pattern → gradually replace legacy components with modern ones while keeping systems running.

Refactor step by step → clean up old code in small chunks to reduce risks and improve performance.

Containerize apps → tools like Docker and Kubernetes isolate workloads, making deployment and scaling easier.

Connect via APIs → use API gateways to let new and old systems talk without deep rewrites.

Test continuously → run automated tests to catch issues early and avoid downtime.

With these steps, you modernize confidently, keeping your operations stable while upgrading to smarter, faster tools.

Alongside tech upgrades, strong data governance frameworks like DAMA-DMBOK ensure your data stays accurate and compliant, which is crucial when dealing with sensitive insurance info. This keeps your operations smooth and trustworthy.

Still, going digital isn’t always smooth sailing. Many insurers run into hurdles like legacy systems or slow adoption. Here’s what’s holding companies back and how to overcome those challenges.

What challenges do insurers face in digitization?

Digitizing insurance processes comes with real challenges, but understanding them will help you tackle them head-on.

You’ll find that cybersecurity tops the list.

Insurers handle sensitive data, so strong security is a must. This means using encryption like AES-256, multi-factor authentication (MFA), role-based access controls, and intrusion detection systems (IDS/IPS). Zero-trust architectures also keep threats at bay by assuming no user or device is automatically trusted.

Next, there’s the complexity of regulatory compliance. You need to navigate laws like GDPR and CCPA, plus insurance-specific rules such as eIDAS and Solvency II. These regulations keep evolving, so staying updated and flexible is key.

Trying to bring new digital tools into old legacy systems can feel like fitting a square peg in a round hole. To smooth this, many insurers use:

Tool type | What it does | Best for | Example platforms |

API gateway | Acts as a single entry point for different systems to communicate securely. | Connecting cloud apps, CRMs, and external services easily. | Kong, Apigee, AWS API Gateway |

Middleware | Sits between systems to translate and route data automatically. | Integrating legacy databases with new digital tools. | MuleSoft, Zapier, Workato |

Enterprise Service Bus (ESB) | Connects multiple enterprise systems with centralized message handling. | Large-scale operations needing high reliability and complex workflows. | IBM Integration Bus, Dell Boomi, WSO2 |

These tools help modernize systems in phases, making the transition manageable. Hybrid cloud adoption also offers a flexible way to scale up digital capabilities without a full overhaul.

Culture-wise, shifting to a digital mindset matters. It’s about agility and teamwork. Frameworks can guide this change. Here are a few that can help shape your digital culture:

SAFe (Scaled Agile Framework) → great for aligning teams, improving collaboration, and managing complex digital programs.

ADKAR Model → focuses on individual change (Awareness, Desire, Knowledge, Ability, and Reinforcement) to help teams adapt smoothly.

Lean Change Management → encourages quick feedback loops and experimentation when rolling out new digital initiatives.

Scrum → ideal for smaller teams running iterative projects with frequent progress reviews.

Design Thinking → keeps your digital transformation customer-focused through empathy, prototyping, and testing.

And, you’ll want to foster data literacy so everyone understands the value of data.

Plus, encouraging continuous innovation through hackathons or innovation labs keeps ideas flowing and teams engaged.

Your workforce will need new skills, too. Think data science, AI oversight, and digital engagement roles. Change management comes into play here, supported by ongoing learning platforms like Coursera and Udemy for Business. These help keep skills fresh and relevant.

Also, solutions like Strada offer enterprise-grade security with SOC 2 Type 2 certifications, customer data isolation, regular penetration tests, and a privacy-first approach in their training data and large language models. These features meet the strict security and compliance standards insurers need.

By tackling these challenges with the right tools and mindset, you’ll navigate digitization in the insurance industry smoothly and successfully.

Once you know the roadblocks (and the way of overcoming challenges in insurance digitization), it’s time to plan your route forward. You’ll learn how to create a clear digital strategy that fits your business goals and helps your teams adapt with confidence.

How can insurers craft a strategic approach to digital transformation?

If you’re ready to “embrace” digitization in the insurance industry, taking a thoughtful, step-by-step approach is key. It’s all about reshaping how your entire organization works to meet future challenges and customer expectations.

Here’s a simple visual to keep your digital journey on track.

And here’s how to build a strong strategy that aligns with your goals and drives measurable results.

Step 1: Assess your digital maturity

Start by understanding where your company stands today.

Use frameworks like the Deloitte Digital Maturity Model to evaluate your current capabilities across technology, processes, and culture.

Here’s how to put it into action:

Assess your baseline. Review where you stand in key areas like strategy, technology, operations, and customer engagement.

Identify gaps. Pinpoint where your digital capabilities fall short, such as outdated tools, slow processes, or low data use.

Prioritize improvements. Focus first on areas that will deliver the biggest business impact, like automation or data analytics.

Set measurable goals. Define clear KPIs, e.g., faster claim turnaround or higher customer satisfaction.

Reassess regularly. Repeat the evaluation every 6–12 months to track progress and adjust your strategy as technology evolves.

This assessment highlights your strengths and gaps, giving you a clear baseline for planning. Think of it as a health check for your digital readiness.

Without this, you risk jumping into solutions that don’t fit or missing critical areas that need improvement.

Step 2: Align strategy with business goals

Next up, sync your digital ambitions with your core business objectives:

Are you focused on improving customer experience?

Reducing claims processing time?

Expanding into new markets?

Make sure your digital strategy supports these goals directly. This alignment ensures every digital initiative adds clear value, avoiding wasted resources on projects that don’t advance your business.

Step 3: Develop a phased implementation roadmap

Trying to do everything at once is a recipe for overwhelm. Instead, outline a phased rollout:

Pilot programs → test solutions on a small scale to learn quickly and adjust.

Scaling → expand successful pilots across departments or processes.

Continuous feedback → keep iterating based on user input and performance data.

This staged approach keeps risk low and momentum high as you grow your digital capabilities.

Step 4: Foster cross-functional collaboration

Digital transformation succeeds when teams work together seamlessly. Encourage collaboration between IT, business units, compliance, and customer service teams.

Using Agile frameworks like Scrum or Kanban can help you stay flexible and responsive. These methodologies promote regular check-ins, rapid problem-solving, and transparency.

Collaborative platforms such as Jira, Confluence, or Microsoft Teams are invaluable here. They keep everyone on the same page, organizing tasks, documentation, and communications in one place.

Step 5: Build a digital culture focused on innovation

Technology alone won’t transform your business. You need a culture that embraces innovation and experimentation. Set up innovation labs or sandbox environments where employees can test new ideas without fear of failure.

Encourage ongoing learning with resources like LinkedIn Learning or Lynda. Upskilling your team continuously equips them to handle new tools and changing workflows confidently.

Step 6: Invest in scalable AI solutions

Start by exploring scalable AI services, such as generative AI from OpenAI GPT models or Google Vertex AI, which can be accessed as a service without heavy upfront development.

For tailored solutions, consider platforms like Microsoft Azure AI or AWS SageMaker to build custom AI models suited to your unique insurance needs. These tools can automate underwriting, claims processing, risk assessment, and more.

For example, if you're looking into practical ways to transform operations with AI, solutions like Strada show how combining AI with workflow automation can boost efficiency and accuracy. If you’re ready to bring AI to life in your insurance operations, here’s a simple step-by-step way to get started with Strada:

Step 6.1: Identify your use cases.

Start small by choosing one or two high-impact areas. Here are a few great use cases to begin with:

Quote intake → capture customer details, qualify leads, and submit data directly into your CRM or AMS.

Renewal reminders → automatically reach out to policyholders before expiration and schedule follow-up calls for your agents.

Claims intake (FNOL) → collect first notice of loss details 24/7, assign adjusters, and trigger next steps instantly.

Payment recovery → follow up with customers who’ve promised payments and send automated reminders if needed.Certificate issuance → process certificate requests automatically and sync updates across your CRM and policy systems.

Lead routing → assign incoming leads based on region, product type, or agent expertise without manual work.

These processes often involve repetitive calls that Strada’s AI agents can easily automate.

Step 6.2: Connect your systems.

Strada integrates seamlessly with your CRM, AMS, and policy systems, so your data flows automatically. Work with your IT or operations team to connect Strada to tools like HubSpot, Salesforce, or Applied Epic using its built-in APIs.

Step 6.3: Configure workflows.

Next, set up your first automation workflows.

Strada Workflows can trigger actions like scheduling follow-ups, sending renewal reminders, or updating CRM records instantly after a call ends.

Step 6.4: Train and test your AI agents.

Use Strada’s onboarding support to train the AI on your product types, call scripts, and business rules. Then, run pilot calls to make sure the responses sound natural and accurate.

Step 6.5: Monitor and scale.

Once live, use Strada’s analytics dashboard to track performance – monitor metrics like call resolution rate, average handling time, and follow-up success.

When you’re confident, expand AI coverage to more lines of business.

In just a few weeks, you’ll see how Strada reduces manual tasks, improves response times, and keeps your agents focused on closing deals instead of chasing paperwork.

Step 7: Prioritize workforce training and performance monitoring

Your investment in technology won't pay off without an informed, engaged workforce. Use digital adoption platforms (such as Whatfix or WalkMe) to provide easy, on-the-job training that helps employees navigate new tools smoothly.

Track progress using analytics platforms like Tableau or Power BI. AI performance dashboards can give you real-time insights into how your AI systems perform, letting you spot issues or opportunities quickly.

Building a digital strategy doesn’t stop at your own systems. The smartest insurers are now connecting with partners (brokers, reinsurers, and tech providers) to share data and innovate together.

Let’s see how these ecosystems work in practice.

How can insurers use advanced data ecosystems and partnerships?

First up, building secure data lakes and warehouses is key.

Platforms like Snowflake and Databricks help insurers gather all types of data – from structured databases to unstructured files like emails or IoT sensor data – into one place. This consolidation makes it easier to analyze and find insights quickly.

Next, collaboration matters. Here’s how to make that collaboration work smoothly:

Use open APIs → allow systems from different partners to communicate securely and in real time.

Adopt standardized data formats → rely on formats like JSON or XML to keep information consistent and readable across platforms.

Implement secure authentication → use OAuth 2.0 or token-based access to protect shared data.

Leverage data exchange hubs → platforms like ACORD or industry-specific data exchanges simplify collaboration between carriers and brokers.

Track data flows → set up dashboards to monitor which partners access what data – keeping everything transparent and compliant.

This openness speeds up insurance customer onboarding digitization and creates a fuller picture of risk. Plus, data marketplaces and open data initiatives expand data sources even more. They bring in fresh, external info that sharpens risk models, making them more accurate.

Some great examples come from partnerships with tech giants. Take AWS Data Exchange and Google Cloud’s insurance programs. They provide curated, high-quality datasets and tools to help insurers innovate faster and smarter. These collaborations act as a bridge to a broader ecosystem where data flows securely and efficiently.

Of course, all this data sharing needs strong frameworks to keep info safe and respecting privacy. Techniques like differential privacy and federated learning let insurers analyze data without exposing personal details. Consent management frameworks ensure customers stay in control of their data.

Finally, platforms like Strada seamlessly fit into this ecosystem. Thanks to open APIs, Strada’s conversational AI insights feed directly into enterprise analytics, CRM systems, or customer data hubs.

This integration helps insurers make smarter, data-driven decisions at every step.

We’ve covered a lot, from new technologies to smarter partnerships. Now, let’s bring it all together and see what the future of digitization means for your insurance business.

How will digitization shape your next move?

Digitization in insurance isn’t just about adopting new tech. It’s about transforming how you work and connect with customers. In 2026 and beyond, the winners will be the insurers who act fast, stay flexible, and put customer experience first.

Here’s how to make it happen:

Start small, scale smart. Pick one process (like claims, renewals, or quote intake) and digitize it first.

Use AI and automation where it matters most. Free your team from repetitive work so they can focus on clients.

Break down data silos. Connect systems through APIs to keep information flowing across departments and partners.

Keep your people on board. Train teams early, communicate clearly, and celebrate small wins.

Measure and adapt. Track KPIs, review progress, and adjust quickly to stay ahead.

Platforms like Strada make this transformation easier. Its AI-driven phone agents automate calls, follow-ups, and workflows, so your team spends more time closing deals and less time on busywork.

Ready to see how it works? Book a Strada demo and discover how automation can help your insurance business move faster, serve better, and grow smarter.

Frequently Asked Questions

What’s the quickest way for insurers to start digitizing without a huge budget?

Begin with small wins—automate one process like renewals or FNOL intake using low-code tools or AI phone agents. This gives fast ROI without major IT overhaul.

How long does a typical insurance digitization project take?

Framer is a design tool that allows you to design websites on a freeform canvas, and then publish them as websites with a single click.

What’s the biggest mistake insurers make when adopting new digital tools?

Framer is a design tool that allows you to design websites on a freeform canvas, and then publish them as websites with a single click.

What KPIs should insurers track to measure digitization success?

Framer is a design tool that allows you to design websites on a freeform canvas, and then publish them as websites with a single click.

How do insurers avoid overwhelming their staff with new technologies?

Framer is a design tool that allows you to design websites on a freeform canvas, and then publish them as websites with a single click.

Table of Contents

Carriers, MGAs, and brokers scale revenue-driving phone calls with Strada's conversational AI platform.

Start scaling with voice AI agents today

Join innovative carriers and MGAs transforming their calls with Strada.

What Is Digitization in Insurance? A Simple Guide for 2026

Amir Prodensky

CEO

14 min read

A straightforward breakdown of digital tools reshaping insurance today.

I still remember when managing insurance policies meant endless paperwork, phone calls, and filing cabinets.

Today, things look completely different.

Digitization has turned all that chaos into clarity. It’s not just about going paperless. It’s about working smarter, faster, and more connected than ever.

Digitization in insurance means using digital tools to improve how insurers operate and serve customers. From AI to automation and data analytics, these technologies help teams make quicker decisions, personalize offers, and deliver better service around the clock.

Why does this matter so much now? Because customer expectations have changed. People want instant answers, simple claims, and personalized experiences, and insurtech startups are raising the bar.

Traditional insurers can’t afford to lag behind.

Digitization helps bridge that gap. It speeds up claims and underwriting, personalizes products, and enables 24/7 support that customers love.

Now that you know what digitization means, let’s look at how it’s changing the insurance world in real time.

How is digitization shaping the insurance industry today?

You’ll be surprised by how much digitization in the insurance sector is transforming everything right now. Across life, health, and cyber insurance, companies are speeding up their digital game.

In fact, 63% of insurers plan to be fully digitized by 2026. The insurtech market is booming, growing rapidly as new technologies reshape how insurers work and serve customers.

What’s driving this shift? It boils down to three key things: customer demand, tougher competition, and new technology.

Customers want faster, simpler service on their phones. Insurers face pressure to keep up with nimble startups and tech-savvy rivals.

Meanwhile, technologies like AI, blockchain, and IoT devices keep opening fresh ways to improve operations. Here are some practical examples of digital tools making a difference today:

Mobile apps that let you manage policies or file claims anytime, anywhere

Chatbots providing quick answers without waiting on hold

Automated underwriting to speed up approvals and reduce errors

Telematics for real-time risk assessment in auto insurance

Blockchain ensuring transparency and security in transactions

These tools boost speed, cut costs, and improve how risks get assessed. They’re also great for spotting fraud faster and keeping customers engaged with personalized experiences.

One standout example is Strada’s AI phone agents. They handle calls 24/7 for things like renewals, first notice of loss (claims intake), policy updates, and customer follow-ups. This not only ramps up efficiency but also helps keep customers happy and loyal.

Simply put, digitization in insurance is making the industry faster, smarter, and more customer-friendly. And if you’re wondering what’s next, expect even smoother, more connected experiences very soon.

So, what’s driving all this change? It starts with the tools behind the transformation. Let’s break down the key technologies that power modern insurance, from AI to automation and everything in between.

What digital technologies are insurers using?

When it comes to digitization in insurance, technology is the engine that drives efficiency, customer experience, and innovation. You’ll find that insurers today rely on a range of digital tools and platforms designed to simplify operations and deliver personalized service faster.

Here’s a straightforward breakdown of the core tech powering this transformation.

1. Artificial intelligence

First up, AI plays a huge role.

It enables predictive analytics that help insurers assess risks more accurately. AI automates underwriting, so policies get approved quicker without compromising quality. It’s also essential for fraud detection, flagging suspicious claims before they cause big losses.

On top of that, AI streamlines claims processing by analyzing documents and data faster than humans can.

2. Robotic process automation (RPA) and intelligent automation

Next, RPA and intelligent automation shave hours off repetitive tasks. These tools handle workflows like:

Data entry → bots pull and update client information instantly. No more manual typing.

Policy renewals → automated reminders and renewals keep customers engaged without staff chasing dates.

Billing and payments → systems generate invoices, send payment links, and confirm transactions automatically.

Document processing → AI scans forms, extracts key details, and files them where they belong.

Customer updates → automated workflows send status emails or texts right after each step.

The result? Happier teams and quicker turnaround times.

3. Chatbots and conversational AI

Customer service has gone digital too.

Chatbots and conversational AI provide 24/7 support for policy questions, claims updates, and onboarding. For example, tools like Artificial Solutions and Lemonade’s AI chatbot engage customers instantly, answering common queries and guiding them through process steps without waiting on hold.

One impressive example in conversational AI is Strada’s platform, which uses insurance-specific AI models trained on industry terminology. It handles calls covering quote intake, lead qualification, renewals, claims, and policy servicing with ease.

Best of all, it integrates smoothly with CRM and AMS systems, creating a seamless experience for both agents and customers.

4. Telematics and IoT devices

If you want real personalization, look no further than telematics and IoT devices. By tracking driving behavior or home conditions, insurers offer usage-based policies that reward safe habits with lower premiums.

Companies like Octo Telematics and T-Sense lead the way here, giving both insurers and policyholders real-time insights.

5. Blockchain and smart contracts

Security and transparency also get a boost from blockchain and smart contracts. These technologies make policy and claim management more secure and transparent by recording transactions on distributed ledgers.

Platforms such as Ethereum-based solutions and IBM Blockchain reduce paperwork and minimize disputes.

6. Digital Adoption Platforms (DAPs)

To help agents get the most from these digital upgrades, many insurers turn to Digital Adoption Platforms like Whatfix. These platforms train employees on new software quickly, improving productivity and encouraging tech use across the board.

7. Cloud, APIs, and modern architecture

Digitization isn’t just about isolated tools. It’s also about how companies plan and deploy them. Many insurers use an AI roadmap approach: identifying use cases, running pilot projects, then scaling successful solutions.

Meanwhile, modernizing legacy systems often relies on API-first architecture, microservices, and cloud-native transformation to increase flexibility. Leading cloud platforms like AWS, Microsoft Azure, and Google Cloud provide the scalability and security insurance companies need.

Of course, technology alone doesn’t make the magic happen.

It’s what you do with it.

Next, we’ll explore how these digital tools are completely reinventing the customer experience, making it faster, smoother, and more personal than ever.

How is customer experience transforming with digitization?

Today, it’s all about a digital-first, omnichannel journey. Instead of sticking to phone calls or in-person visits, you can now manage your policies through mobile apps, online portals, and self-service tools anytime, anywhere.

For example, platforms like Policybazaar and Insurify make comparing policies and buying insurance simple and quick without the usual hassle.

And this shift goes beyond convenience. AI is stepping in to make things smarter and more personalized. Here’s how it’s changing the game:

Predictive insights → AI anticipates customer needs, like when they’re likely to renew or file a claim.

Smarter pricing → machine learning adjusts premiums based on real behavior and risk data.

Instant service → chatbots and AI assistants provide quick, accurate responses 24/7.

Tailored offers → algorithms match customers with the right products in seconds.

Faster decisions → AI analyzes documents and verifies information automatically, cutting delays.

With AI working behind the scenes, every interaction becomes faster, more accurate, and far more relevant to each customer. Plus, AI-powered recommendation engines suggest the best policies suited to your needs.

Dynamic pricing adjusts costs based on real-time data, making sure you get competitive deals. Natural language processing (NLP) and sentiment analysis help understand your questions and feedback more accurately, offering faster, tailored responses that keep you engaged.

Now, here’s where it gets really useful: digitization speeds up service. You can submit claims in real-time just by uploading images or videos from your smartphone. No more waiting in lines or mailing documents.

Digital signatures mean you can sign contracts instantly, without printing a single page. To make digital signatures part of your everyday workflow, here’s a quick step-by-step guide:

Step | What to do | Why it matters |

1. Choose a platform | Pick a trusted tool like DocuSign, Adobe Sign, or HelloSign. | Ensures legal compliance and security. |

2. Upload your document | Add contracts, policies, or claim forms directly from your computer or cloud storage. | Saves time and centralizes files. |

3. Add signature fields | Drag and drop where signatures, initials, or dates should appear. | Makes signing clear and easy for clients. |

4. Send for signature | Email the document securely to your client or team member. | Cuts delays from printing, scanning, or mailing. |

5. Track progress | Get instant notifications when someone signs or opens your document. | Keeps you informed and speeds up approvals. |

6. Store and sync | Save completed documents automatically in your CRM or AMS. | Keeps records organized and easy to retrieve. |

Need advice? Many insurers offer virtual consultations via video directly integrated into their portals – helpful and hassle-free.

Another game-changer is chatbots and conversational AI. These tools provide 24/7 support, answering common questions anytime, helping you avoid hold times or searching through FAQs.

Strada is a great example of this transformation in action. They offer zero-hold-time phone service and smart call scheduling with intelligent retries, which means you get connected faster and more often. Their personalized, trusted interactions boost customer loyalty and keep you coming back.

Here’s what makes Strada stand out in everyday use:

Faster connections → calls route instantly to the right agent or AI assistant; no waiting.

Smarter follow-ups → missed calls trigger automatic retries and reminders, so no lead slips away.

Personal touch → AI tailors conversations based on customer history and preferences.

Consistent support → works 24/7 across phone and SMS, so customers always get help when they need it.

Happier teams → agents handle fewer repetitive calls and focus on high-value interactions.

Together, these features turn every call into a smooth, personalized experience, boosting satisfaction, efficiency, and long-term loyalty.

Which brings us to design. Insurers are making their apps and websites easier to use. They follow proven UX/UI frameworks like Material Design or Human Interface Guidelines, so everything feels intuitive and smooth.

Plus, they continuously improve features using agile methods and DevOps to keep you satisfied and reduce the chances you’ll switch providers.

With these changes, insurance digitization is not just about technology. It’s about making your experience easier, faster, and more personal every step of the way.

You can really see the difference when you look at the customer journey itself. Here’s what that evolution looks like in action.

But it’s not just customers who benefit. Digitization also transforms day-to-day operations, cutting manual work and boosting efficiency.

Let’s see how insurers are using digital tools to streamline claims, underwriting, and servicing.

How does digitization improve insurance operations?

You’ll be amazed at how digitization turbocharges insurance operations.

First, by automating manual tasks, insurers cut claims processing times drastically, from around 30 days to less than 15. This speed-up doesn’t just make customers happier; it also lowers human errors and helps spot fraud faster.

For example, AI-powered tools like Shift Technology and FRISS analyze patterns to catch suspicious claims early, protecting your bottom line. Next up, AI improves underwriting and risk assessment by digging into mountains of historical data.

No matter if it’s predicting the impact of natural disasters or profiling health risks, AI algorithms provide sharper, data-backed insights.

This means better pricing accuracy and smarter decisions in less time.

Digitization also brings RPA into play through platforms like UiPath and Automation Anywhere. These bots handle repetitive tasks such as document sorting, claim form parsing, and workflow approvals.

One standout tool is Strada Workflows – an AI platform that instantly turns call outcomes into automated actions across CRM, AMS, and policy systems. It streamlines tasks like renewals follow-up, claim file creation, payment recovery, and certificate issuance to reduce busywork and boost your team’s productivity.

Plus, NLP helps machines understand insurance documents and customer communications, speeding everything up through insurance document digitization without sacrificing accuracy.

Here’s a simple list of key automation benefits you’ll see:

Faster claims and policy workflows (with insurance policy digitization)

Reduced manual errors and fraud detection

Smarter risk assessment and underwriting

Lower operational costs from less manual labor and cloud infrastructure savings